On paper, the sheer volume of announced industrial work in Louisiana is unprecedented—pegged by economists at as much as $140 billion since 2012. In reality, the number of projects to break ground could be somewhat lower, should market conditions maintain their current trajectory.

“This is an expansion like none we’ve seen before and I’ve been watching this state for years,” says economist Loren Scott of Loren C. Scott & Associates. “In the past, if we had $5 billion in industrial announcements, we would’ve thought that was a good year. It’s something that we’ve never seen before. It’s an amazing number.”

However, of the $140 billion in projects, less than half—$65.3 billion—have broken ground, and some industrial contractors grumble that the work may never materialize as a downturn in oil and a strong dollar negatively impact the bottom lines of many industrial companies. This is particularly evident in Baton Rouge, where the work appears to have crested.

Scott says it’s a matter of timing and project delays. “Some of the projects are working through the permitting and financing stages, and in some cases you’re seeing actual delays,” he adds. In the New Orleans MSA (Metropolitan Statistical Area, stretching from St. James to Plaquemines parishes), only $3 billion of its $24.6 billion in announced projects is currently underway. And in Lake Charles, about half of its $93 billion in announced projects has broken ground.

In the current oil-price environment, the New Orleans and Lake Charles MSAs stand to lose the most, since the majority of their projects are in the design stage. In particular, St. James Parish could suffer the greatest impact—a majority of the announced projects in the New Orleans MSA are concentrated there.

Where do we go from here?

Beyond 2017, industry experts say the crystal ball gets hazier, with the impossible-to-predict price of oil and the Asian economies playing critical roles in determining the course of future industrial development. One thing is clear: It would be overly optimistic to expect all current announced work to materialize or to expect that a similar surge in announced work will occur again anytime soon.

Until recently, natural gas prices—a key input for capital decisions—had been a major catalyst for expansion. While natural gas traded at about $2 per million BTUs in the U.S., it had not dropped significantly in Europe and Asia, where natural gas is more closely tied to the price of oil.

“This was to our advantage when the price of oil was over $100 a barrel, and these countries were having to pay $15 for their natural gas,” Scott says. “In that environment, there’s no way they could possibly compete with us.”

It’s a different story today, as significantly lower oil prices have made overseas gas prices more competitive.

David Dismukes, executive director of the Center for Energy Studies, says the demand side of the equation will be equally important in coming years. Most eyes will be focused on Asia, where the market is expected to contract over the next few years, thereby lowering the need for commodity chemicals.

“I think in 2017 and beyond we’ll continue to see opportunities, but the size and scope of that is going to be a function, almost entirely, of what’s going on with the global economy,” Dismukes says. “Growth is the challenge, and that works against everybody, not just Louisiana.”

He points to concerns that the Asian markets are undergoing long-term structural changes, and that China, specifically, is seeking to re-orient itself from a market focused on rapid growth to one more consumer driven. “If that’s the case, then you’re not going to see 8% to 12% growth anymore,” Dismukes adds. “You’re looking more at 4% to 7% growth a year. That changes your dynamics. That’s going to push out the window for new commodity chemical capacity until 2020.”

As an unfortunate result, the need for new projects won’t be there.

Scott contends that natural gas prices will be the most significant predictor of future investment and growth in industry. “You’re not going to have to worry about the price of natural gas here—because we are awash in it,” Scott says. “We have more natural gas than we know what to do with. The question is what’s the price of natural gas going to be in Europe and Asia. That’s the key.”

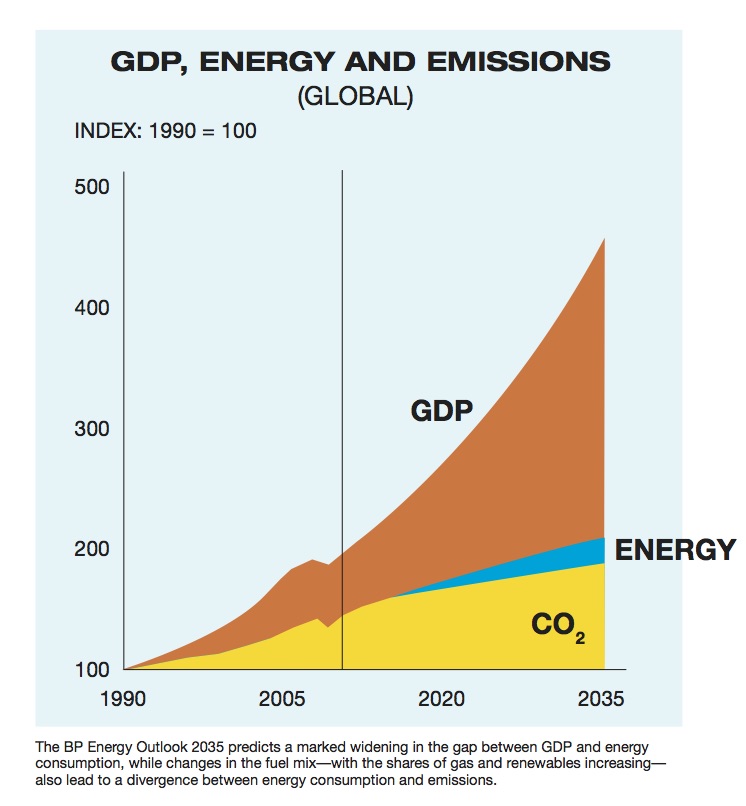

In fact, the impact of natural gas prices on industrial development should increase for years to come. Speaking at LSU’s Center for Energy Studies in March, BP economist Mark Finley predicted natural gas would be the fastest growing fossil fuel through 2035, spurred by strong supply growth—particularly of U.S. shale gas and liquefied natural gas (LNG)—and by environmental policies.

He added that while natural gas dependency will increase, overall energy consumption won’t match overall GDP growth due to improvements in technology. “While world GDP is expected to more than double, unprecedented gains in energy efficiency will mean that the energy required to fuel the higher level of activity will grow by only about a third,” he adds. BP’s Energy Outlook 2035 offers 20-year projections on a worldwide scale, based on “most likely” assumptions for energy demand.

Environmental regulation

Apart from unknowable factors such as a worldwide recession or depression that would “clearly cause a reduction in the demand for chemicals,” Scott points to a tightening of air quality standards as having a potentially negative impact on industrial competitiveness.

This would be largely influenced by who occupies the White House in 2017. A Hillary Clinton or Bernie Sanders win, Scott says, would undoubtedly lead to heightened standards that could dampen expectations and competitiveness.

In particular, the EPA’s Clean Power Plan would increase the cost of power and negatively impact the industrial market’s bottom line should it come to pass.

“If power plants are required to shift to natural gas, wind or solar power, the impact is going to be a significant rise in utility rates,” Scott says. “[Industrial plants] are huge users of electricity. If the Clean Power Plan is fully implemented, industrial utility rates could go up 48% in Louisiana.”

Subsequently, an increase in rates would prompt owners to look to invest in other countries.

Greg Bowser, executive vice president of the Louisiana Chemical Association, says the Clean Power Plan, as it stands, could be problematic for the industry, although LCA has not taken an official stand on the issue.

“It will drive up energy costs, we believe, and so that’s going to be a problem for our industry,” Bowser says. “We’ve agreed to listen, to take a look at it and run it through our process internally with our membership to see exactly what it will do to us.”

State budget

Another worry is that the state’s current budget crisis will ultimately make Louisiana’s primary competitor—Texas—more attractive for future investment.

“We need to understand that the decision about where to locate a plant is largely a matter of math,” Scott says. “You sit down and you figure out your internal rate of return, and if you come along and say that you’re going to solve the budget crisis by levying a sales tax on electricity then that becomes part of the equation.”

While resolving the current budget crisis is a priority, Scott says the state could “kill the goose that laid the golden egg.”

While resolving the current budget crisis is a priority, Scott says the state could “kill the goose that laid the golden egg.”

On the plus side, economists say Louisiana’s 10-year tax exemption, Quality Jobs Program and Certified Sites Program (at Louisiana Economic Development) are necessary programs that provide competitive advantages over neighboring Texas. “The fact that we’ve got $143 billion worth of announcements indicates that we’re doing a good job of staying competitive with them,” Scott adds. Other obvious advantages are low-cost natural gas, the Mississippi River and a well-developed system of ports.

Still, Dismukes says, “It’s not like we’ve got it hands down and we can dictate terms to industry. People can move. They might want to get closer to other sources of gas and other basins like in Ohio and Eagle Ford in Texas. I don’t think people are going to pick up plants and leave, but when they start making marginal decisions about continued expansion, these are some things to consider.”

LCA’s Bowser says it’s a certainty that an unfavorable tax policy in Louisiana would lead to a shift of industry to Texas and other regions, if measures are taken that make the state less competitive from a tax standpoint. “I understand that we need to change some things in our tax structure, but we can’t be so out of whack with our neighboring states that it leads to a slowdown in investment.”

Bowser fears the current administration is looking at short-term fixes while not considering the potential long-term damage.

“We’re not saying you don’t need to do some things; we think you do,” he adds. “But we can’t do things that have long-term negative impacts on our economy. Especially right now, when our oil and gas industry is already suffering from low oil prices. The last thing we want to do is start putting obstacles in the way.”

Outlook: Baton Rouge and New Orleans

In Baton Rouge, Scott predicts a noticeable drop in new industrial announcements and construction in 2017 and beyond, given current known variables. Additionally, many significant projects will be completed this year or the next.

“The drop in construction employment will be somewhat offset by new permanent jobs created by the plants, but it takes more people to build plants than it does to operate them,” Scott says. “So you’re going to see a little downward pressure on the Baton Rouge MSA’s employment.”

Conversely, the potential in New Orleans is for good, solid growth beyond 2017 “if the potentials become actuals.” These projects will lead to a bump in construction employment, particularly in St. James Parish.

The work in New Orleans will come at a fortunate time for Baton Rouge-headquartered construction firms who can make the short drive down I-10 for work. “Performance, Cajun, Turner and others are heavily involved in construction all along the 10/12 corridor,” Scott says. “The folks at these companies are still doing pretty well, but they’re also nervous because there’s so much potential out there that has not yet gone vertical.”

Outlook: Lake Charles and the LNG Market

At a minimum, construction employment should remain stable in the Lake Charles MSA, if not grow slightly, should projects—particularly in the LNG sector—pull the trigger and go vertical.

“A huge part of [southwest Louisiana’s] numbers are the LNG export terminals,” Scott says. “There are at least seven projects announced in the area, and two of them have gone vertical—Cheniere Energy and Sempra Energy.”

The remaining projects—totaling about $50 billion—are still in design or have been delayed.

“The problem is that because the price of oil has dropped down to $40, we no longer have a competitive advantage in selling natural gas,” Scott says. “For the most part, they don’t have these 20-year contracts [as they did before]. Therefore, there are billions of dollars in capital investment that are going to depend upon the price of oil getting back up again, and back up pretty quick, for these folks to be able to pull the trigger.”

Consequently, because of Lake Charles’ high concentration of LNG export facilities, predicting future employment numbers there is more difficult.

Originally published in the second quarter 2016 edition of 10/12 Industry Report.